About the author

If you are entering into work on a contractual basis it can often be confusing as to how this affects your tax situation. Should you be paying regular levels of PAYE and NI or corporation tax like a limited company? Lower taxes are an obvious advantage to working on your own terms but it is possible that HMRC will still see you as someone’s employee even if you believe yourself to be completely independent.

IR35 legislation was introduced in 1999 to prevent people from setting themselves up as independent contractors as a means to avoid tax and it has been a major headache for anyone working to contracts ever since; causing a number of employment experts calling for it to be modified or scrapped. That said, George Osborne mentioned the “suitability” of IR35 in his recent autumn budget so it appears this tricky piece of legislation is here to stay.

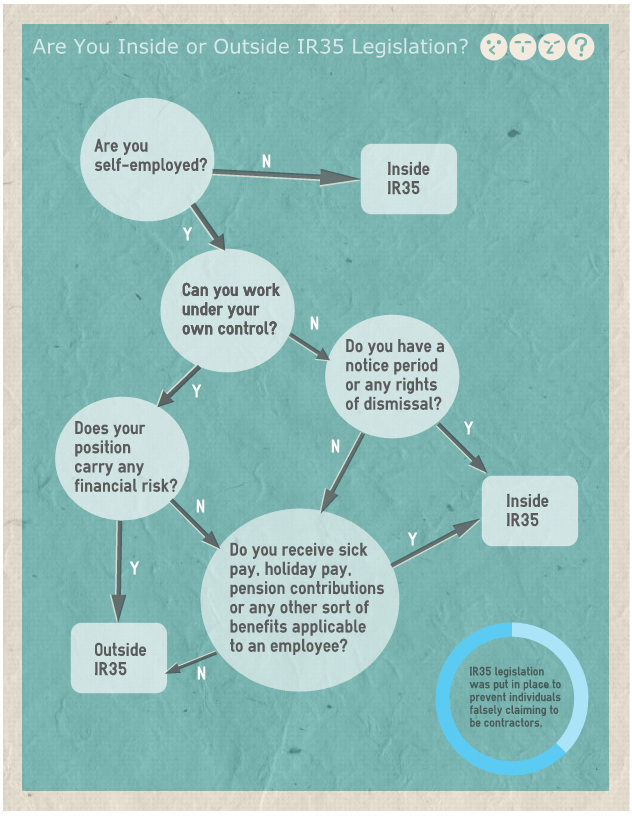

An individual can be deemed inside or outside IR35 based on a number of factors. To be found “inside” IR35 would mean HMRC regard you as an employee and to be found “outside” would mean HMRC consider you independent.

Infographic supplied by The Accountancy Partnership

To be outside IR35 all of the following should, typically, apply:

- You should be your own boss

- You should be financially responsible for your works completion and quality

- You should provide your own tools and equipment

- You should be paid a set amount for a specific job

- You should not have any benefits that an employee enjoys (sick pay, pension contributions etc..)

If a contract you enter does not conform to the above guidelines then it is possible that HMRC will deem you an employee and due to pay regular income tax. HMRC does admit there is grey area in IR35 though, so if you are unsure of a contract check it over with a small business advisor or a contract accountant.

If HMRC do believe you have not paid appropriate levels of tax for work carried out they can reclaim a percentage of the amount due pending an investigation.

Have you had any other issues with Tax? Comment below.

Like what you're reading? Subscribe to our top stories.

{kind=link}